Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

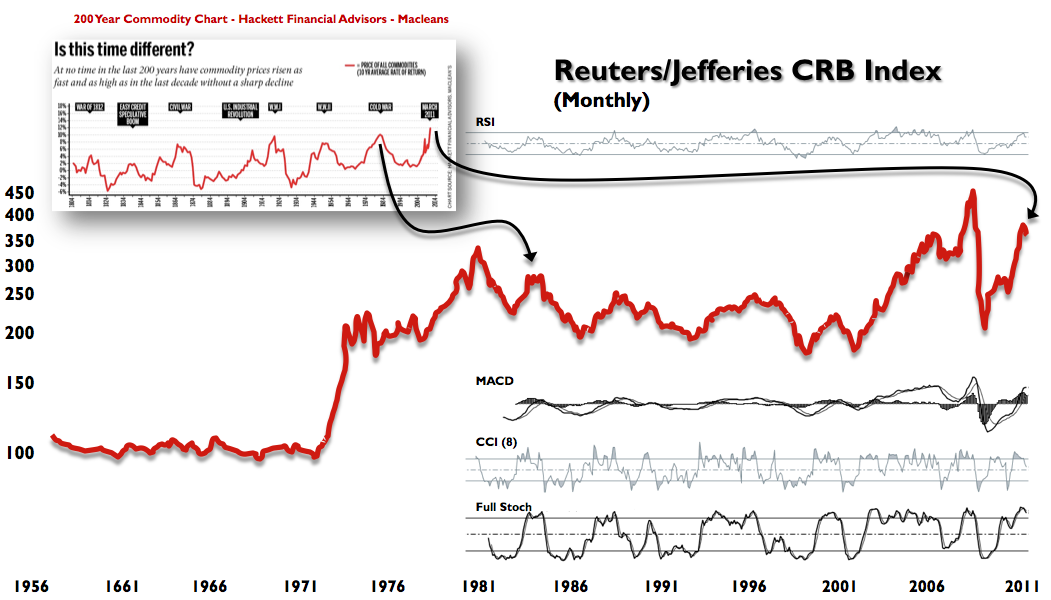

– Our economy through tremendous gains in productivity (and accounting) has transitioned to profitability at such a historically high petroleum and commodity cost multiplier, that by dialing energy and commodity prices lower here through the relative tightening (no additional QE) of monetary policy could in fact provide the most comprehensive stimulus to the economy and the consumer – just when the Fed was perceived to have no additional rounds left in the chamber. To think that even five years ago before the financial crisis hit, that the US economy would be able to maintain the degree of profitability it has exhibited today (with over 9% unemployment, a 12% output gap and until last week – $100 oil) would have been perceived as pure academic fiction. No economist in their right mind would have believed that these economic conditions could have produce such results. –