Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

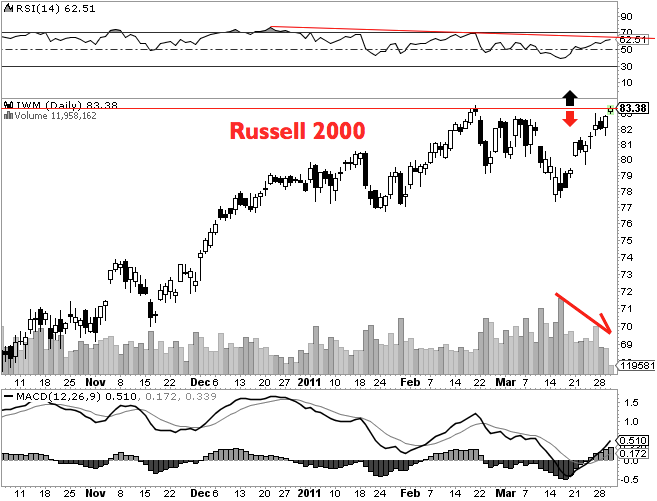

Divergence

A quick intraday update, considering the charts are revealing some divergences about the market in here. Apologies if I am simply applying the KISS method of TA for these charts. However, I do believe Einstein once said, “Everything should be made as simple as possible, but not simpler”. Here’s hoping to finding that balance.