For the better part of the past year, I have maintained a bearish perspective towards what was once one of the more favorable corners of the market – the precious metals sector; more specifically – silver. This was largely due to a confluence of conditions, namely;

1. The extreme outperformance of silver versus gold through the first half of 2011,

2. Major pivots in both the U.S. Dollar and the Euro, and

3. The underperformance of China’s equity markets

And while I am still skeptical of silver and gold’s prospects as well as our own equity markets over the longer term, their immediate prospects look quiet compelling – should the price and momentum patterns unfurl as I believe they may.

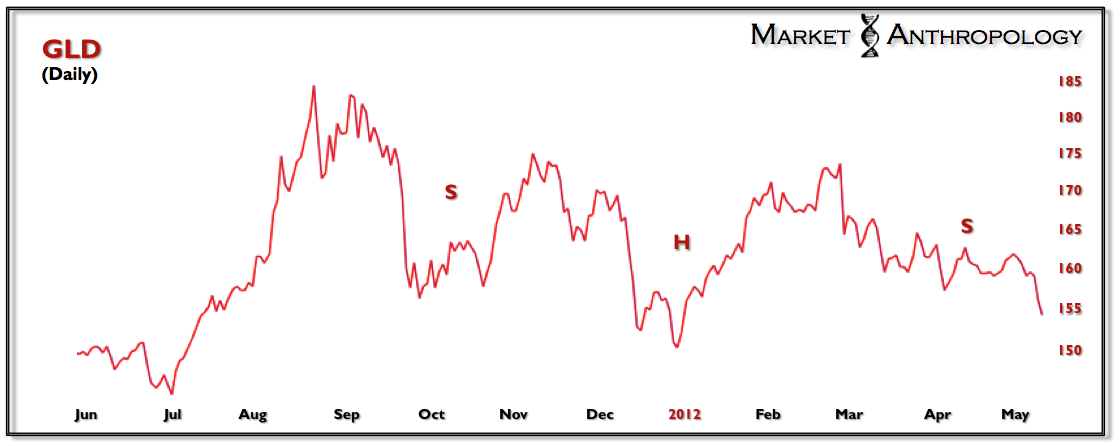

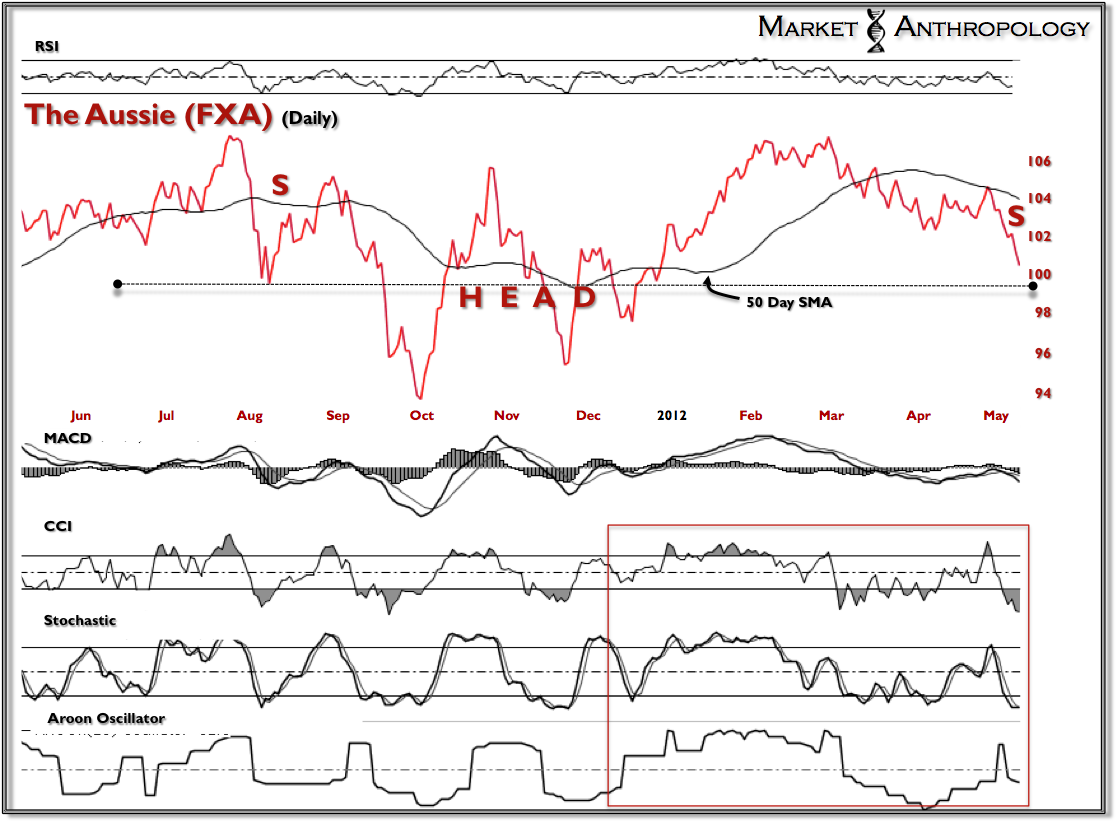

Essentially, many of the key asset proxies that comprise the risk on/off formula – gold, silver, the silver:gold ratio, the Australian Dollar and the Shanghai Stock Exchange, all present distinctly inverted head and shoulders patterns, as well as secondary momentum signatures, that indicate to me – a violent reversal is approaching in the coming sessions.

Leading the way, the Shanghai Stock Exchange has already completed the right shoulder of its inverted head and shoulders pattern. Not surprisingly, the silver:gold ratio has trended very closely over the past several years with China’s appetite for risk. I believe the silver:gold ratio, after completing its contractual agreement with structure – will continue to follow the SSEC, which should put a tailwind behind both the equity and precious metals markets going forward.

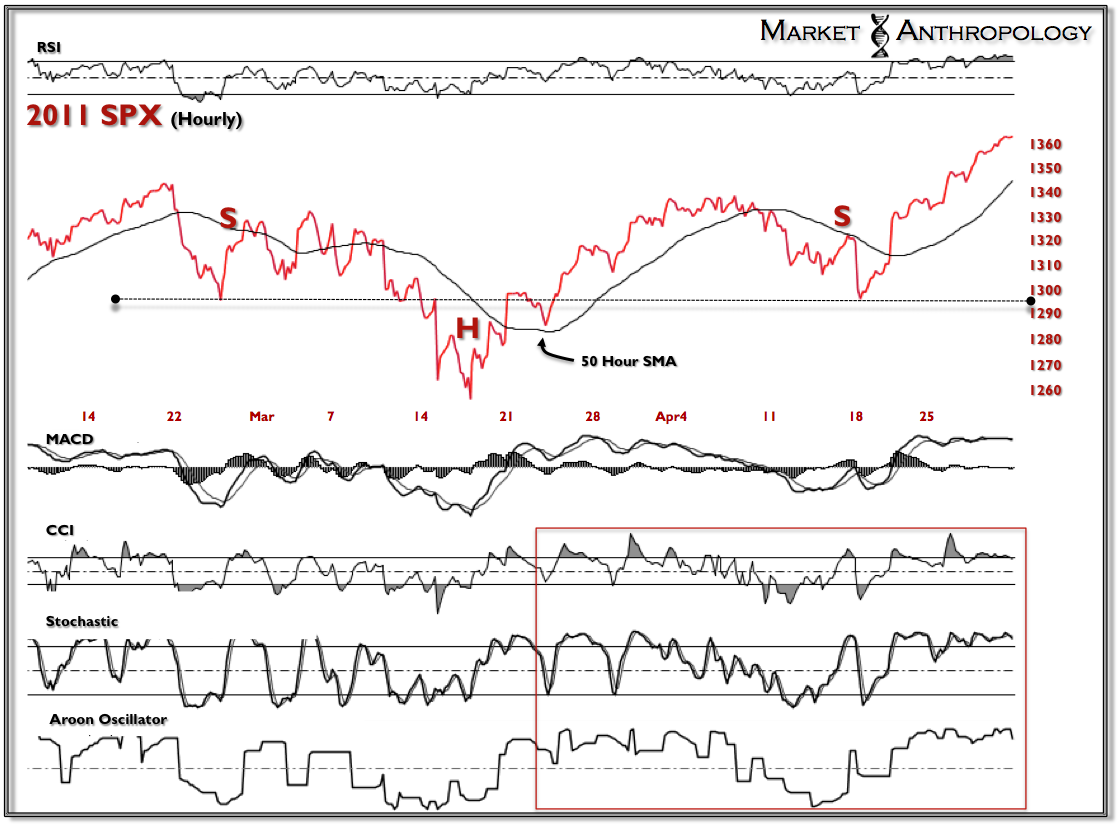

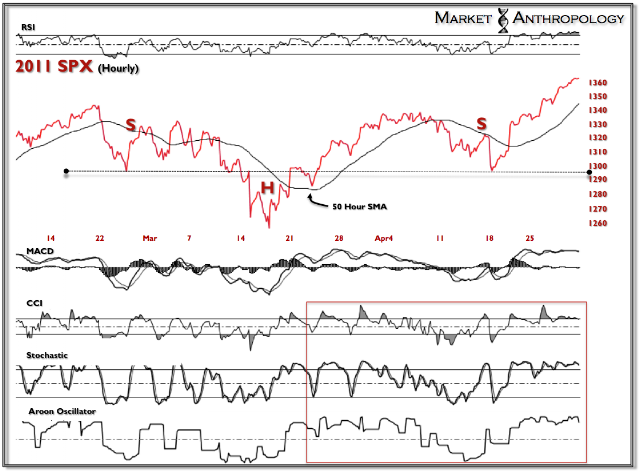

All of the assets mentioned above have momentum profiles very similar to the inverted head and shoulders chart of the SPX from last year. I believe we will see a similar reflex trajectory develop as we spring out of the bear trap that is the right shoulder of the respective patterns. Shanghai has already made the turn, the remaining assets should follow in the coming days.

Considering where the equity markets and these bellwether assets are currently situated – it may be the first year in three where “Sell in May” is no longer the perennial market maxim.

As always – stay frosty.