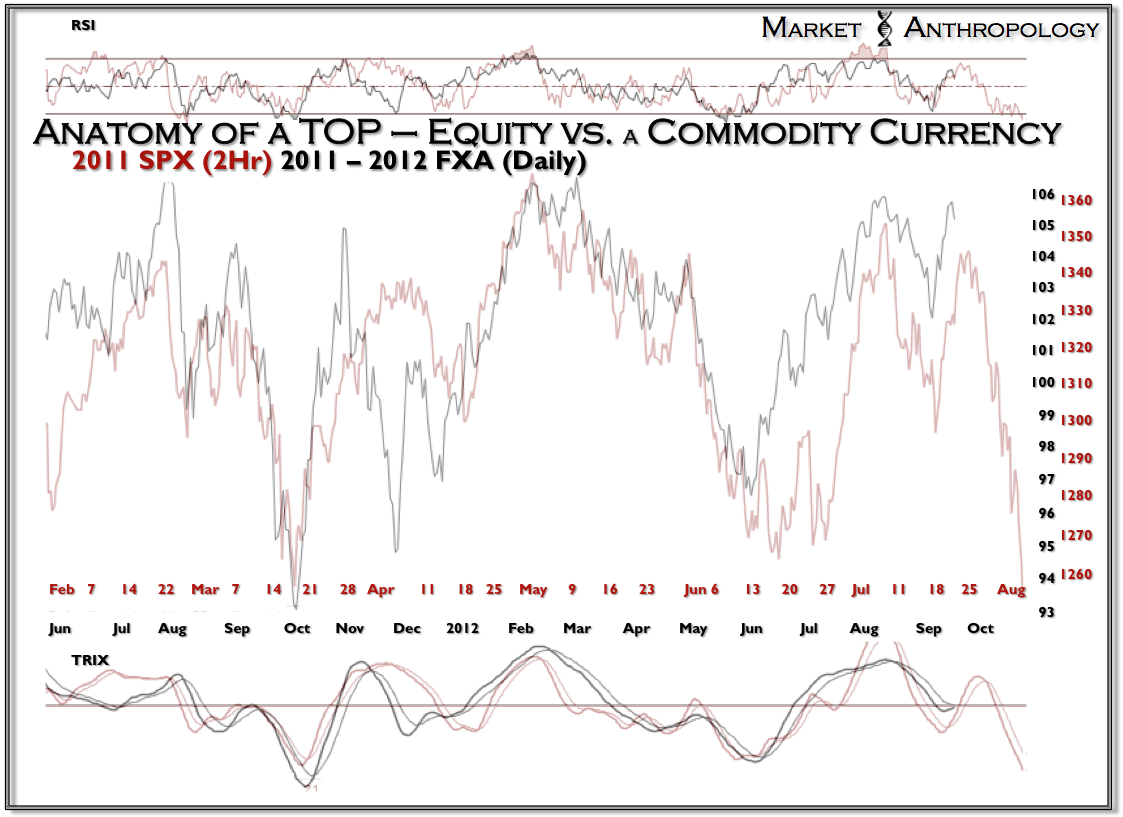

Granted, the markets were always bi-polar – even before the Fed started fluxing its capacitor and attempting to bend the continuum. Bewildering though – in recent years, as we have travelled between the carrots and the sticks, and the parallel monetary universes of Europe and the US – that the markets have become downright schizophrenic to the long term and material impact of QE on the equity, commodity and currency markets. As traders, many of us try and hold several perspectives in our heads at any one given time. However, the Chairman’s influence and practical real-time disruption of market trajectories through the promise, then delivery of QE – has amplified that thought process into an almost dissonant chorus of outcomes and kinetics.