With the debate continuing on whether the domestic equity markets are stretched at another historic extreme, we thought we would take a variant look at the fundamental metric many have voiced their opinion on recently – that being, Robert Shiller’s cyclically-adjusted price-earnings (CAPE) ratio. While we would echo the esteemed Professor’s remarks that the ratio shouldn’t be used to market time crashes or make short-term trading decisions, we view the series with broad appraisal of form, flow and proportion – and then in comparative perspective with the current market environment to glean any potential insights.

As much as the 29′ vintage or even the 37′ tape scares up the most headlines and eyeballs these days, there is a historic analog (one that we are fairly certain no one references and few remember, sans Cashin), that does resemble traits of the current market environment from several different metrics and measures – e.g. yields, valuation, asset cycle, Fed policy and even post-war strategic posture.

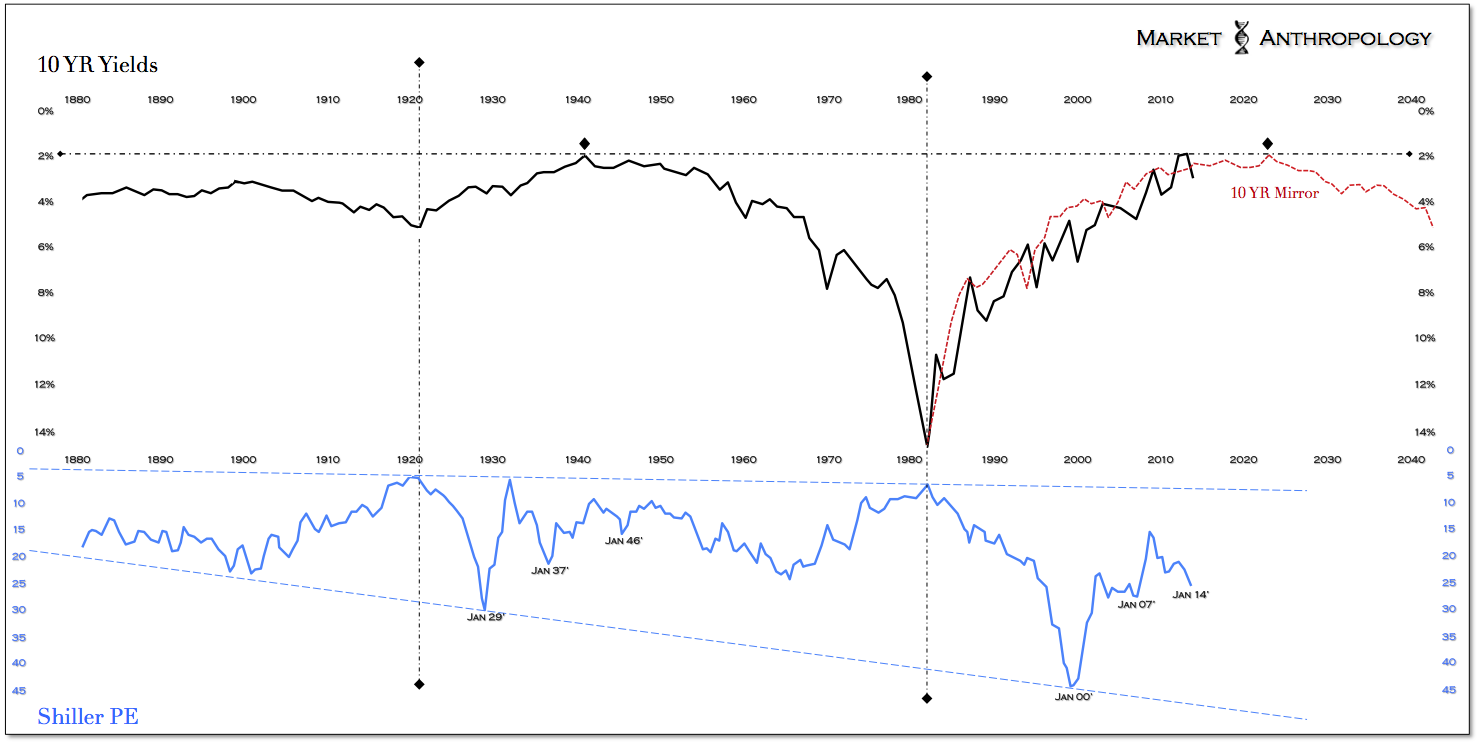

However, what really brought us to the 46′ parallel, was simply looking at the CAPE ratio on a longer-term horizon and with reference to the yield/rate cycle – which we would argue primarily drives the boat from a valuation and asset cycle perspective.

Click to enlarge images

All data courtesy of www.multpl.com and based on yearly data as found on January 1st of each year

A few observations between the two series charted above:

- The exhaustive highs in the yield cycle (21′ & 82′) corresponds to the valuation troughs in the ratio.

- The valuation range of the ratio is proportional to the size of the long-term interest rate cycle. I.e., the greater yields were pulled (higher) – the higher the valuation range was subsequently extended. To this point, we note the congruences and timing between the two broader cycles – with the yield peaks made in 21′ and 82′ (Jan 1st data) and the lagged reflex and explosive drive higher of the ratio directly following the pivot lower in yields. Yields rose for ~ 20 years leading up to the peak in 21′ and the equity market subsequently exploded higher for ~ 8 years leading up to the 29′ high. In the most recent cycle, yield rose for ~ 40 years to a peak in 82′ and the equity markets enjoyed the historic disinflationary open road for ~ 18 years leading up to the valuation peak in 00′.

- One way to look at the kinetics, correlation and lag between the series is that the ratio correlates with the yield and rate cycle for a period until higher yields and inflation expectations put downward pressures on equity prices, thus creating the pressure differential described above that’s eventually released with proportional inertia subsequent to the cycle high in yields.

- Similar to what is found in other wide-angle asset panoramics (see Here), the relative range of Shiller’s PE isn’t static, but broadening with a rising lower and upper range. We would argue the drift higher in valuations is primarily a result of the expanded range of the current yield cycle.

- As often the case with major crashes, the outlier effect to the broader cycle does muddle the interpretive tea-leaves forward. Having said that – and although they didn’t occur at the same point or present with equal magnitude (33′>09′), we view the extended dislocations from the equity market crashes (29-33′ & 08-09′) as relative outliers with respect to the ratio calculation – but view them nonetheless with wide peripheral vision to the broader flow and bearings of equity valuations within the respective cycle. Moreover, it doesn’t make much sense to us to compare absolute valuations between cycles – because of how the ratio is calculated based on a smoothed 10 year inflation-adjusted metric and the difference in size and magnitude between the respective yield/inflation cycles.

Although the metric is very close to the valuation peak in 07′, we would view a pivot lower this year as this cycle’s equivalent to the ratio’s historic trend through 46′.

This perspective is supported by similarities in:

- The long-term yield backdrop – which is the mirror for the current downtrend in rates.

- The monetary environment of the 1940’s – which saw the Fed purchase and hold all available short-term U.S. treasuries and virtually all long-term U.S. Treasuries – a greater percentage of outstanding securities than what the Fed owns today.

- The composite equity market performance since the previous ratio lows in 42′ and 09′.

- The pivot higher in the commodity markets this year, which was also dramatically evident when the Fed pivoted from its outright purchase of securities in the market at the end of 45′ and which helped refresh inflation expectations and extended the commodity cycle to its cyclical high in 51′.

How Russia, the Ukraine or the new Twitter diplomacy fits into the equation is anyone’s guess. But if you needed any more spurious evidence – the 46th parallel does run straight through Crimea…