Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

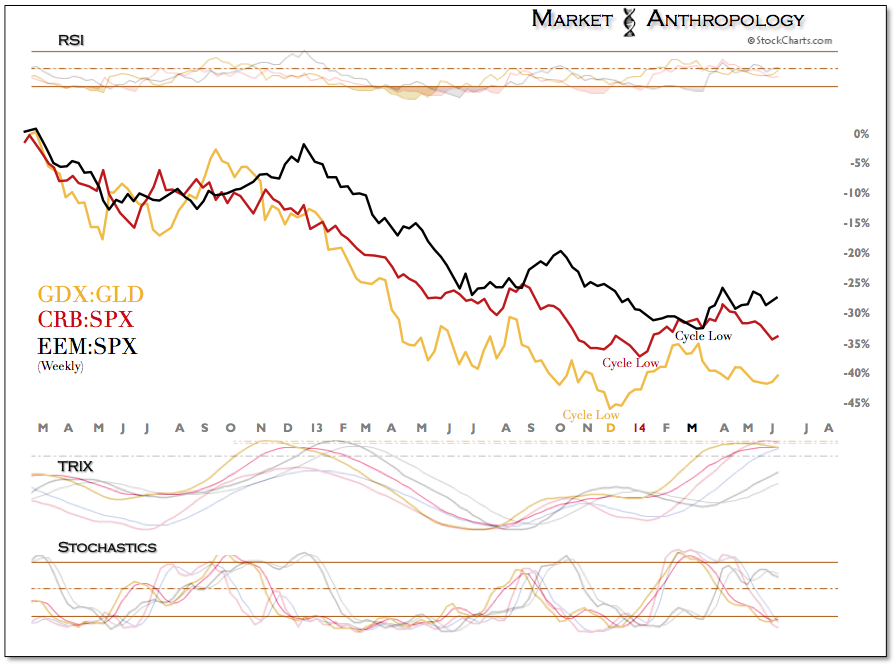

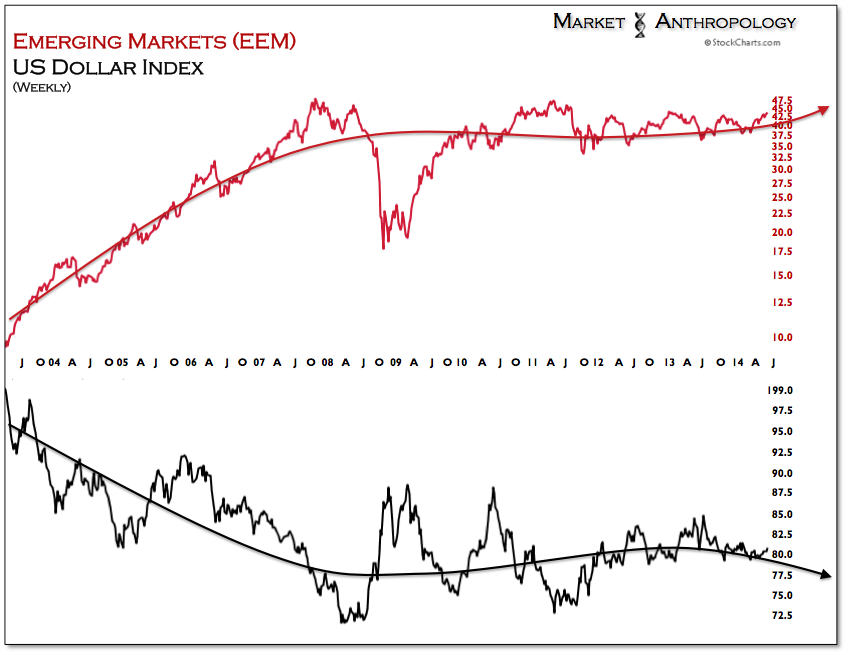

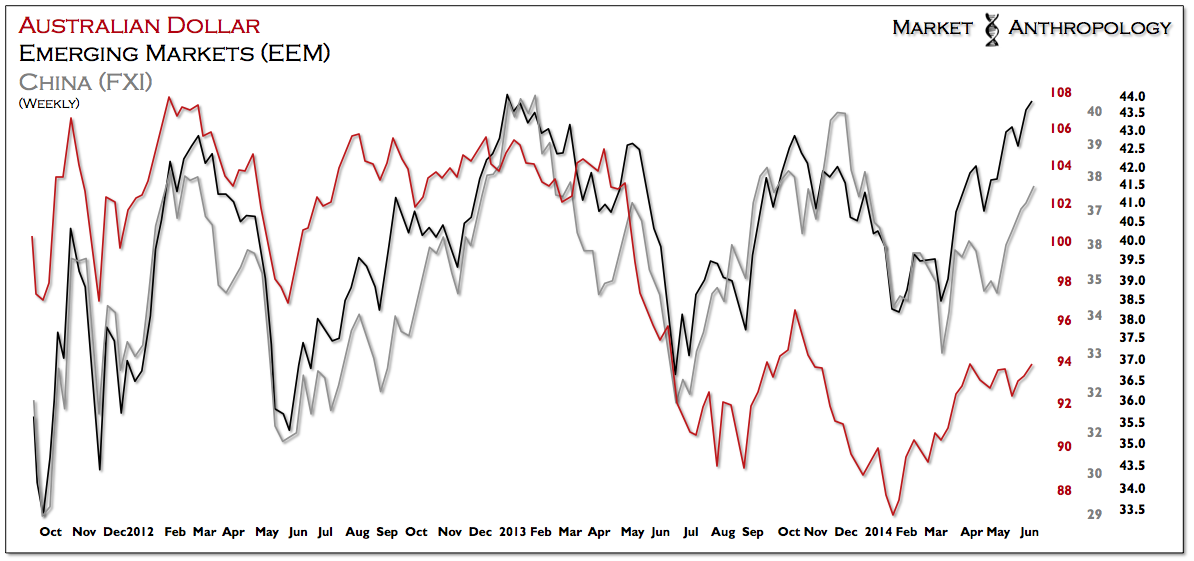

Lost in the soundbites of 19 record closes for the S&P this year and 9 for the Dow – is the backstory that the commodity sector and long-term Treasuries have still outperformed both indexes. While the darlings of the Dow and S&P might receive the headlined attention year-to-date, we continue to feel last years class of ugly ducklings still hold the most promise and potential going forward. Broadly speaking, this class includes emerging market and Chinese equities, the precious metals sector and commodity currencies closely associate with such strength. As we pointed out throughout this year, what they all have in common from a macro perspective is a disposition for outperformance when real yields decline.

Lost in the soundbites of 19 record closes for the S&P this year and 9 for the Dow – is the backstory that the commodity sector and long-term Treasuries have still outperformed both indexes. While the darlings of the Dow and S&P might receive the headlined attention year-to-date, we continue to feel last years class of ugly ducklings still hold the most promise and potential going forward. Broadly speaking, this class includes emerging market and Chinese equities, the precious metals sector and commodity currencies closely associate with such strength. As we pointed out throughout this year, what they all have in common from a macro perspective is a disposition for outperformance when real yields decline.

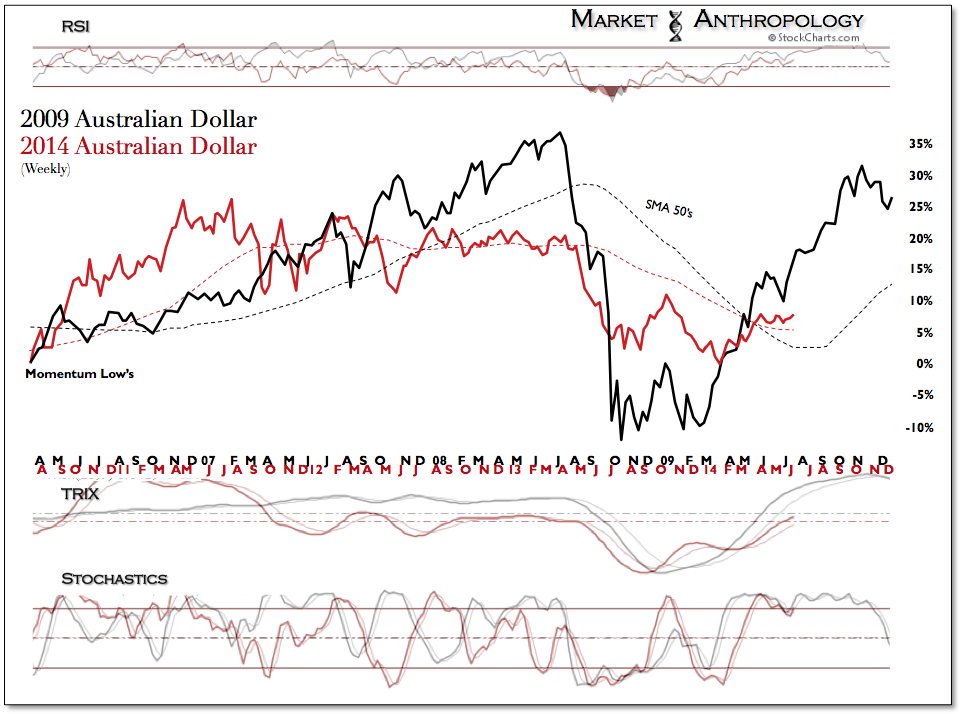

We’ve held a favorable opinion on the Australian dollar throughout this year and expect the Aussie to make its way back to trend line resistance extending from the early 2013 highs and away from paralleled support which extends from the pre-crisis highs in 2008.

We have utilized the momentum and performance comparative from the 2008 waterfall decline as a prospective profile for the Aussie today. Similar to our work with TIPs this year, the currency has followed the broader pivots of its historic retracement structure. Should the comparative remain prescient, we expect the Aussie to take the next stair higher over the coming weeks.

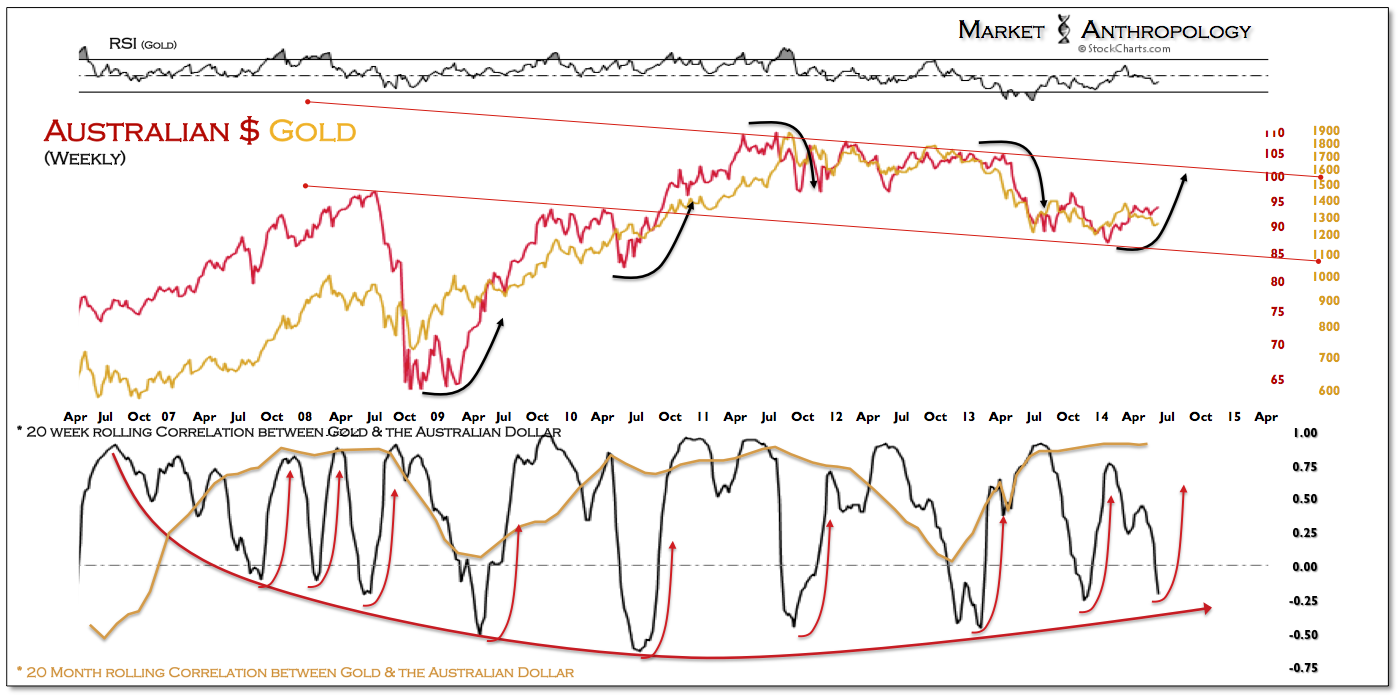

We have also followed the strong positive correlation relationship that exists between the Aussie and silver and gold. In the past we have made note of the lagged correlation along shorter timeframes between precious metals and the Aussie. While the relationship between assets has ebbed and flowed when measured against daily and weekly timeframes, expressed along a monthly horizon the correlation between the Aussie and precious metals has strengthened since 2007.

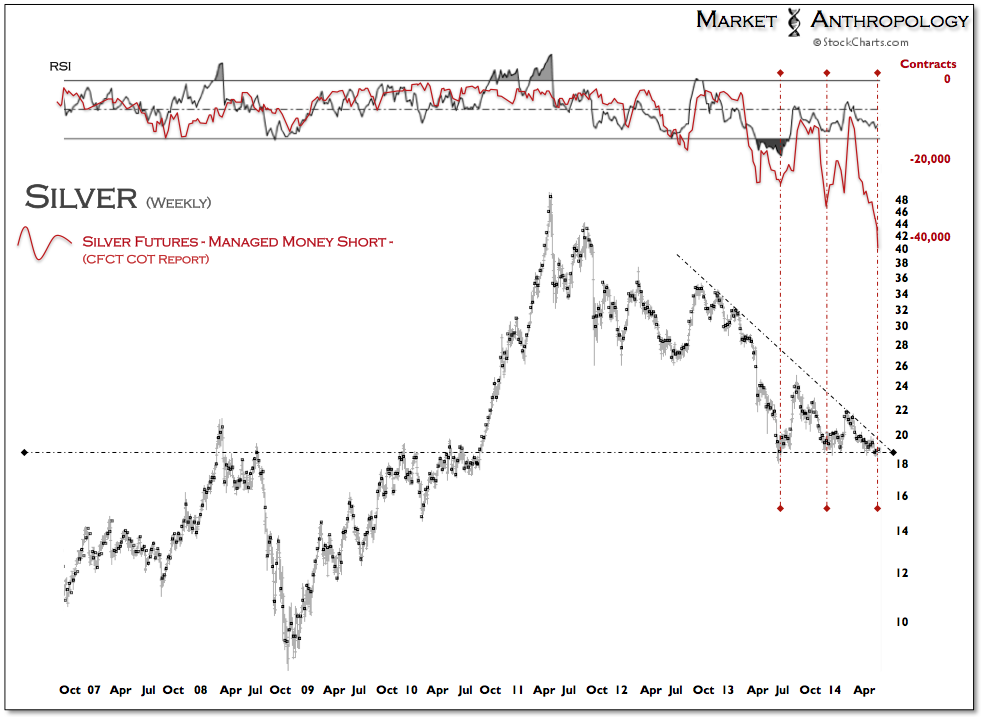

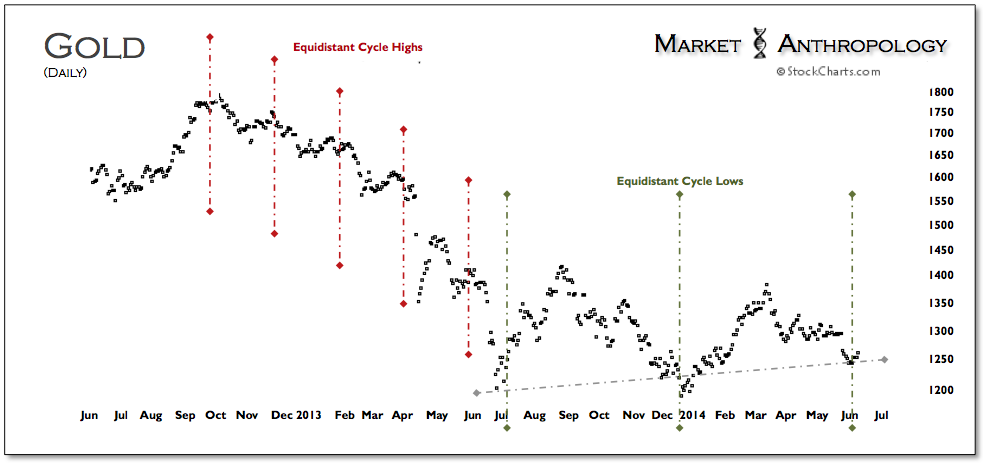

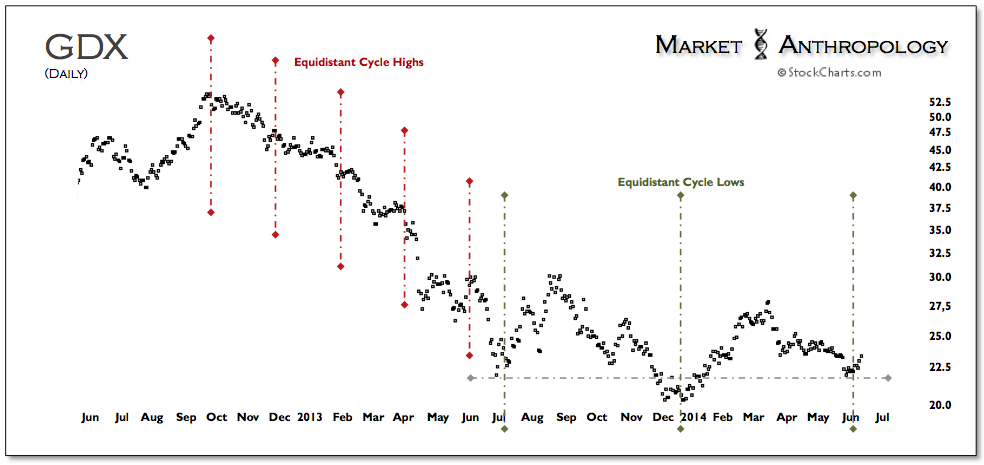

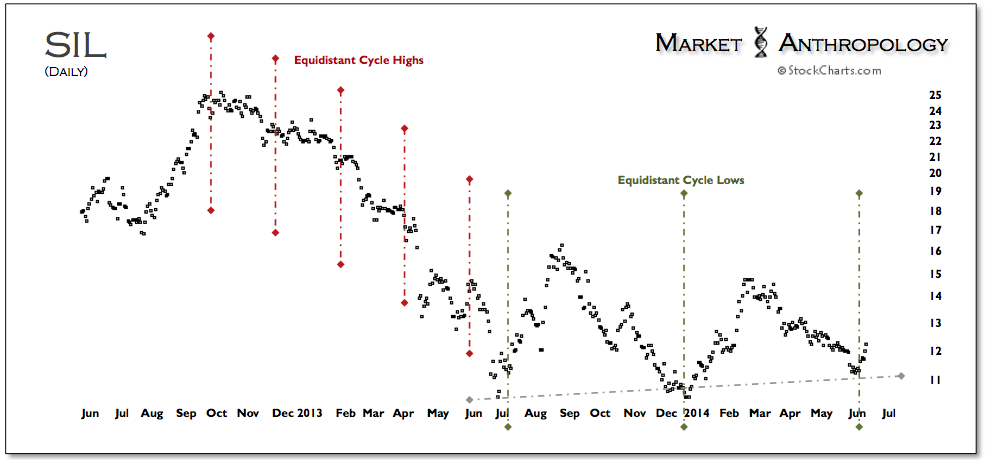

With gold and silver on the precipice of taking their first steps higher from the nearly year long consolidating range, we expect the correlation relationship with the Aussie to pulse positive once again through the daily and weekly timeframes.

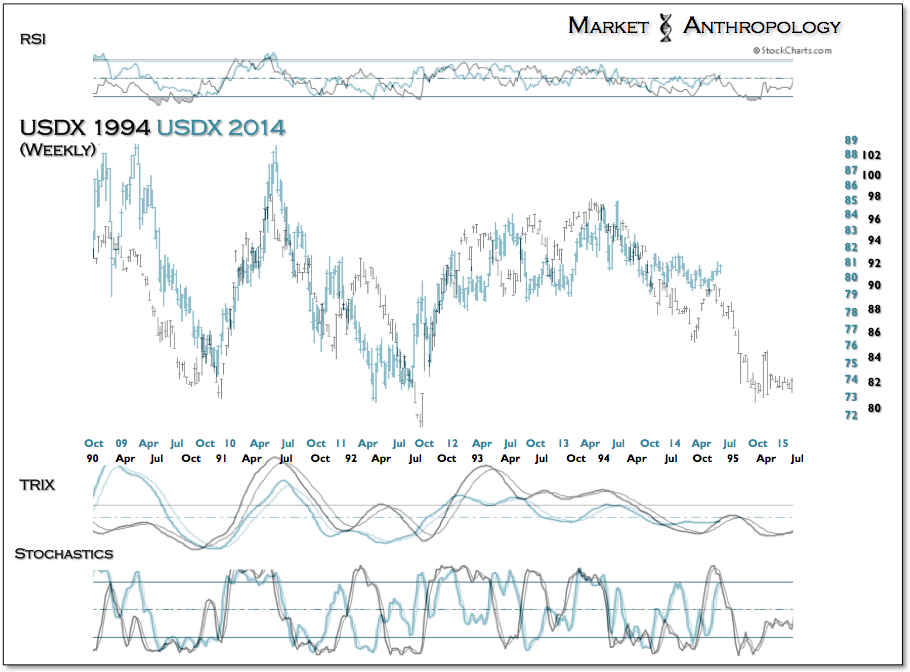

As we previously mentioned, the commonality between the above trends and assets is a strong sensitivity to inflation expectations and long-term yields. From our perspective, real rates are poised to continue falling, as we expect long-term yields and the US dollar to broadly decline – while another pulse of inflation moves through the system.

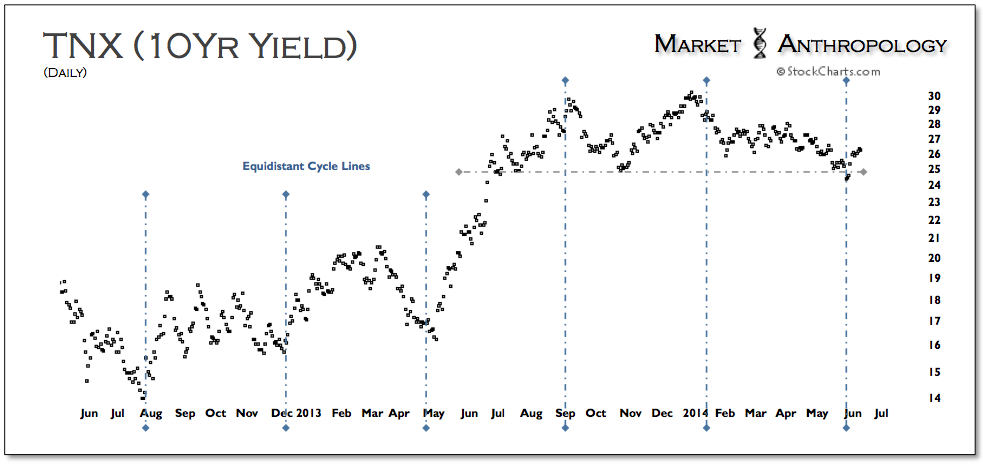

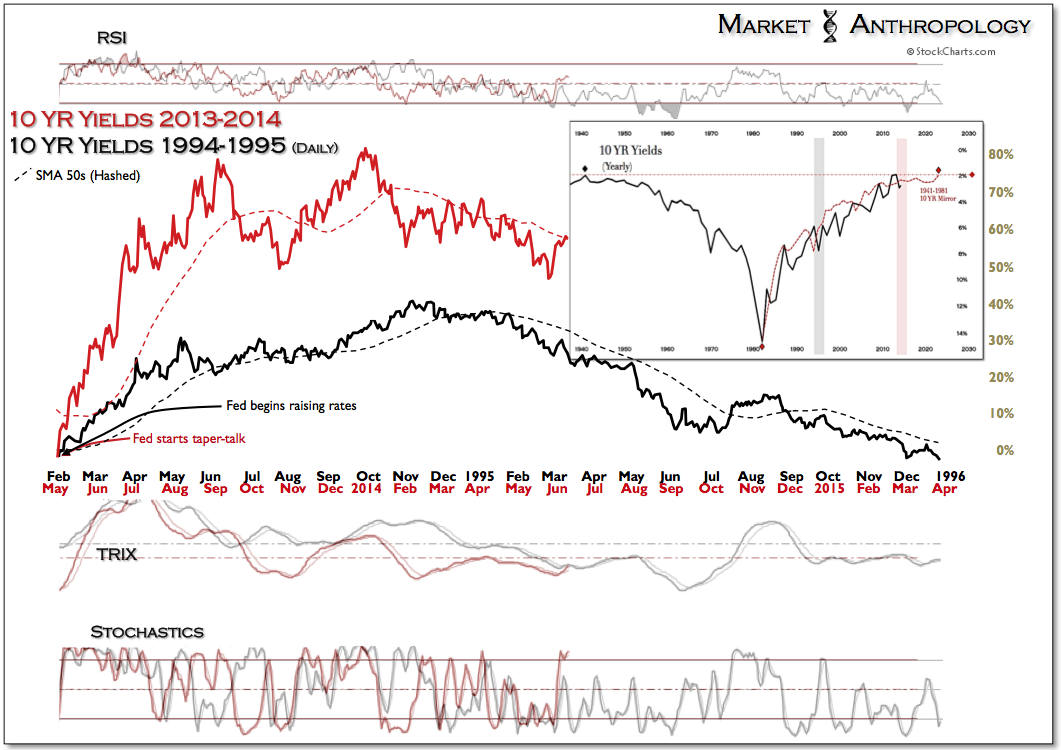

These atypical market conditions were predicated by the relative extreme reach in 10-year yields last year while inflation expectations troughed and firmed. As expected, we have seen the reflexive move in long-term yields reverse, while inflation expectations have continued to improve.

{kind=link}