Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

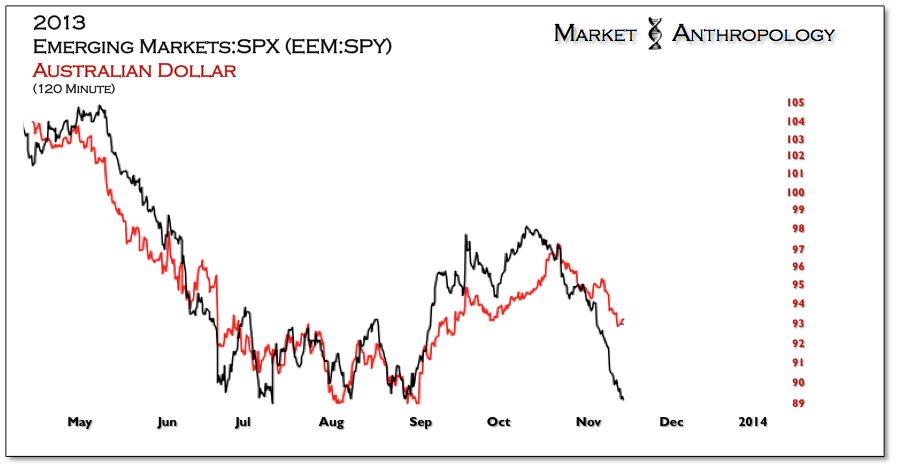

From a comparative perspective, it appears the Aussie took the expedited path for this retracement decline. In either case, we would be looking for a healthy bounce to reappraise.

Rounding things out is an update of our 2011 BKX comparative with the miners that continues to point towards a prospective breakout for the group in the balance of the year.