Skip to content

Popular

You Say Tomahto I Say Tomato

Jelly of the Month Club

586 Billion Caution Flags

Where the Wild Things Are

About

Physical Address

304 North Cardinal St.

Dorchester Center, MA 02124

Facebook

Twitter

Instagram

Pinterest

YouTube

Partners

Press

About

Useful

Facebook

Twitter

Instagram

Pinterest

YouTube

Search

Popular

You Say Tomahto I Say Tomato

Jelly of the Month Club

586 Billion Caution Flags

Where the Wild Things Are

About

BUY CRYPTO

Menu

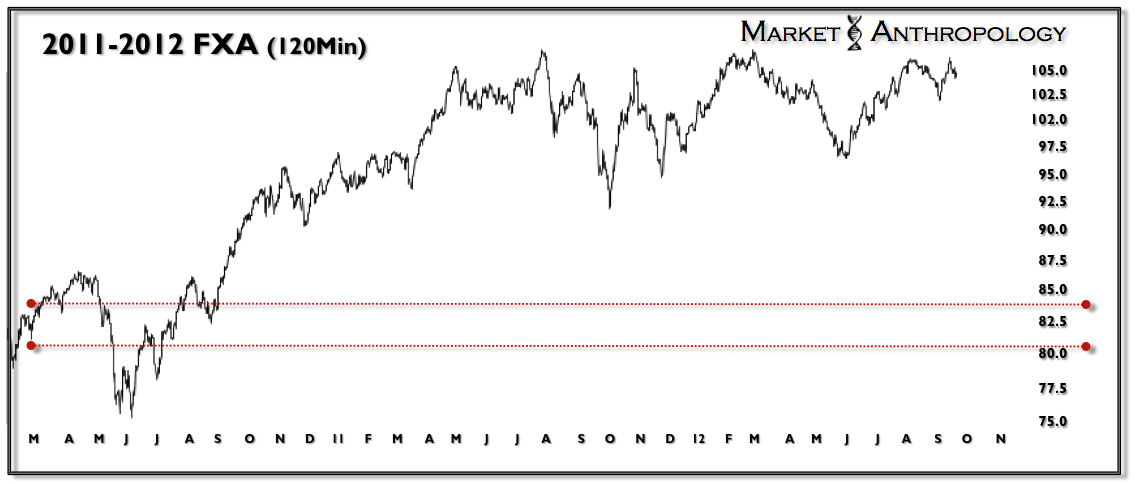

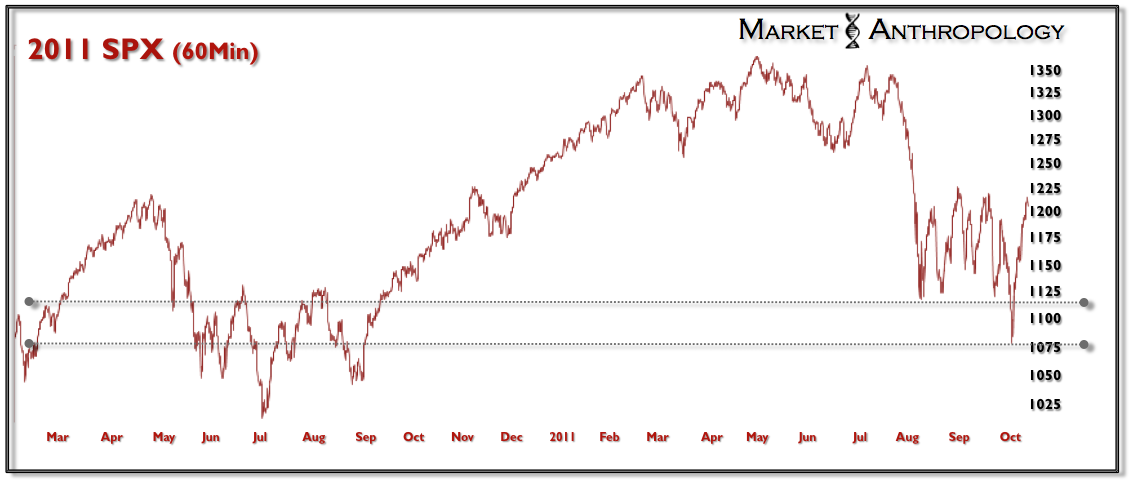

Market Anthropology: Legends of the Fall

admin

August 23, 2021

General

,

Uncategorized

Friday, September 21, 2012

Legends of the Fall

Newer Post

Older Post

Home

Trending now

Market Anthropology: You Say Tomahto I say Tomato

Market Anthropology: the 1335/1340 Hinge

Market Anthropology: the 1440 Interchange

Market Anthropology: 1800 or Bust